Purchasing new equipment is one of the biggest investments a business can make. Whether you're adding a tow truck, replacing heavy construction equipment, expanding your manufacturing operation, or upgrading restaurant equipment, the right financing solution can help your business grow without draining your cash reserves.

That's where equipment leasing comes in.

But before signing any lease agreement, it's important to understand exactly what the lease terms mean. Many business owners focus only on the monthly payment, overlooking critical details that affect ownership, flexibility, taxes, and the total cost of financing.

Understanding equipment lease terms helps you make smarter financial decisions and choose a financing solution that supports your business—not one that creates unexpected challenges later.

In this guide, we'll explain:

- What equipment lease terms are

- How commercial equipment leases work

- Common lease structures

- End-of-term options

- Payment schedules

- FMV leases vs. $1 Buyout leases

- Tips for negotiating better lease agreements

- How to choose the right financing option for your business

Whether you're financing your first piece of equipment or expanding an existing fleet, this guide will help you make a confident, informed decision.

What Are Equipment Lease Terms?

Equipment lease terms are the conditions that define how your equipment financing agreement works from beginning to end.

These terms outline:

- How long you'll lease the equipment

- Your monthly payment amount

- When payments begin

- Who is responsible for maintenance and insurance

- What happens if you pay off the lease early

- Whether you can purchase the equipment at the end of the lease

- What your options are when the lease expires

Think of your lease agreement as the roadmap for your financing. Every clause impacts how your business uses the equipment and what your long-term costs will be.

Unlike a traditional bank loan, equipment leases can be customized to fit your company's cash flow, seasonal revenue, and growth goals.

Why Equipment Lease Terms Matter

The right lease agreement can improve cash flow, preserve working capital, and provide flexibility as your business evolves.

The wrong lease structure can leave you paying for equipment long after it has stopped generating value.

For example:

A Construction Company

A contractor purchasing a new excavator may benefit from seasonal payment schedules that align with project income. Lower payments during slower months help maintain healthy cash flow while keeping projects moving.

A Tow Truck Company

A towing business adding another rollback truck may choose a lease that allows ownership at the end of the term, ensuring the vehicle remains part of the fleet for years to come.

A Manufacturing Facility

A manufacturer investing in CNC machinery may prefer lower monthly payments today while preserving capital for hiring employees, purchasing raw materials, or expanding production.

Each business has different financial goals, making it essential to choose lease terms that match how the equipment will be used.

Benefits of Equipment Leasing

Equipment leasing has become one of the most popular financing solutions for businesses because it provides flexibility without requiring a significant upfront investment.

Some of the biggest advantages include:

Preserve Cash Flow

Instead of spending hundreds of thousands of dollars upfront, businesses can spread equipment costs over predictable monthly payments while keeping cash available for payroll, inventory, marketing, and operations.

Access Newer Equipment

Leasing makes it easier to upgrade to newer technology as your business grows, helping improve productivity and reduce downtime.

Flexible Payment Options

Many equipment leases offer customized payment schedules based on seasonal revenue, delayed project payments, or installation timelines.

Potential Tax Benefits

Depending on your business structure and current tax laws, lease payments may provide tax advantages. Always consult your accountant or tax advisor for guidance specific to your situation.

Faster Equipment Acquisition

Many financing approvals happen much faster than traditional bank loans, allowing businesses to put new equipment to work sooner.

Industries That Frequently Use Equipment Leasing

Equipment leasing supports businesses across nearly every industry.

Some of the most common include:

- Construction

- Transportation

- Towing and Recovery

- Waste Management

- Manufacturing

- Landscaping

- Agriculture

- Healthcare

- Restaurants

- Municipal Services

- Warehousing and Logistics

- Tree Care

- Excavation

- Utilities

- Oil and Gas

- Concrete and Asphalt Contractors

From skid steers and dump trucks to CNC machines, trailers, commercial kitchen equipment, and software systems, leasing helps businesses acquire the tools they need without tying up valuable capital.

Common Types of Equipment That Can Be Financed

Businesses can finance a wide variety of equipment, including:

- Tow Trucks

- Rollback Trucks

- Dump Trucks

- Vacuum Trucks

- Sewer Inspection Equipment

- Hydro Excavators

- Bucket Trucks

- Box Trucks

- Semi Trucks

- Excavators

- Dozers

- Skid Steers

- Loaders

- Forklifts

- Manufacturing Equipment

- CNC Machines

- Packaging Equipment

- Medical Equipment

- Restaurant Equipment

- Commercial HVAC Systems

- Trailers

- Modular Buildings

- Office Equipment

- Computer Hardware

- Software Systems

At First Financial LLC, we help businesses finance both new and used equipment across a wide range of industries, offering customized financing solutions designed to fit each customer's needs.

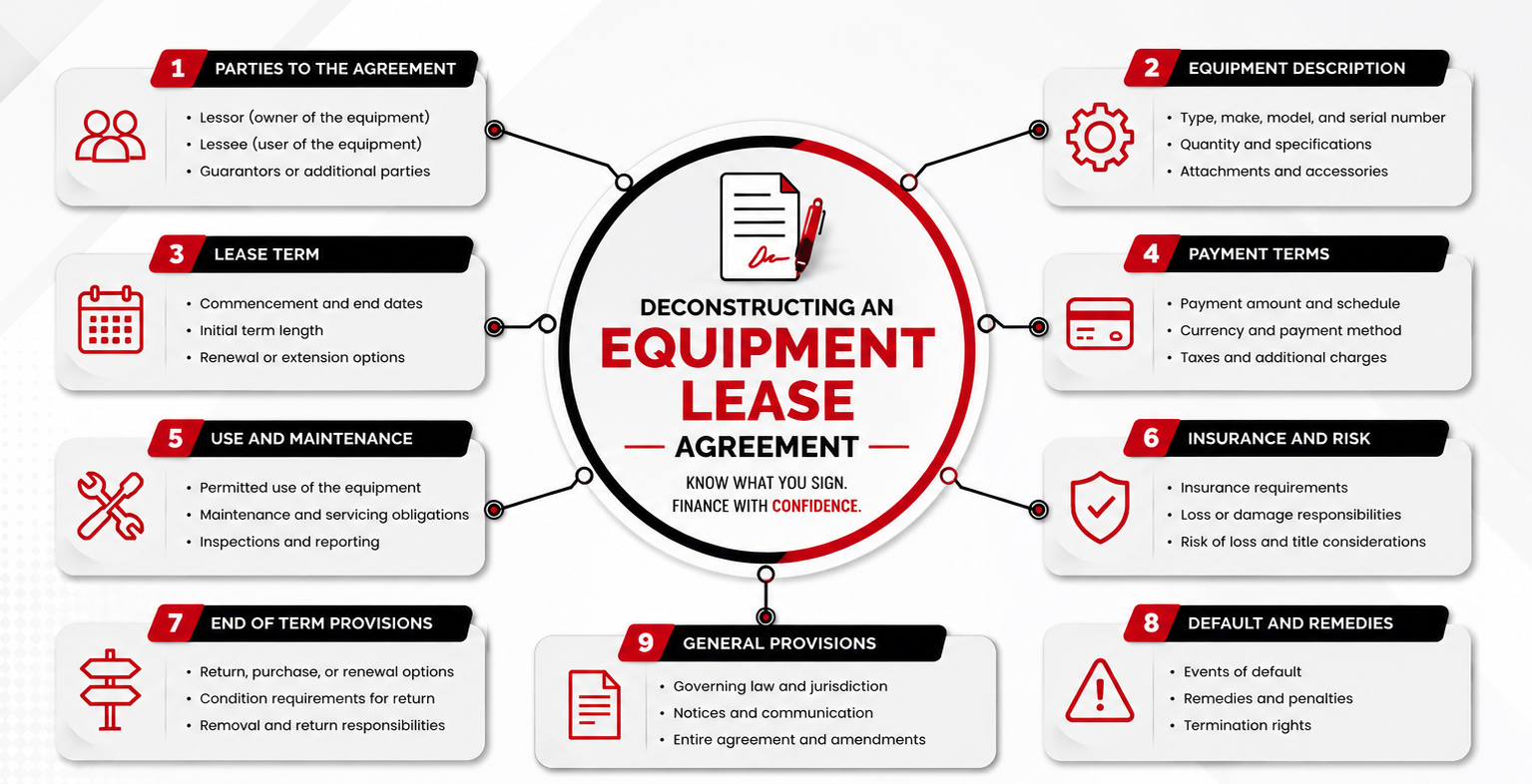

Understanding Equipment Lease Terms: Lease Length, Payment Structures, and End-of-Term Options

Choosing the right equipment lease isn't just about finding the lowest monthly payment. The structure of your lease can have a significant impact on your business's cash flow, flexibility, and long-term financial goals.

Before signing any equipment financing agreement, it's important to understand how lease terms work and how different options can affect your business.

Fixed-Term vs. Month-to-Month Equipment Leases

One of the first decisions you'll encounter is the length of your lease. Most commercial equipment financing agreements fall into one of two categories: fixed-term leases or month-to-month (periodic) leases.

Fixed-Term Equipment Leases

A fixed-term lease has a predetermined length, typically ranging from 24 to 84 months, depending on the type of equipment being financed.

This is the most common lease structure for commercial equipment because it provides predictable monthly payments and allows businesses to budget more effectively.

Fixed-term leases are ideal for:

- Heavy construction equipment

- Tow trucks

- Commercial trucks

- Manufacturing machinery

- Agricultural equipment

- Waste and recycling equipment

- Medical equipment

If you know you'll need the equipment for several years, a fixed-term lease often provides the best value.

Month-to-Month Equipment Leases

Month-to-month leases offer greater flexibility but are less common for large commercial equipment purchases.

These agreements may be appropriate when:

- Equipment needs are temporary.

- You're testing new technology.

- A short-term project requires specialized machinery.

- You expect your equipment needs to change quickly.

While they offer flexibility, month-to-month leases may come with higher monthly costs and less predictable long-term expenses.

How Lease Length Affects Your Monthly Payment

Many business owners assume that selecting the longest lease available is always the most affordable option. While longer lease terms generally reduce monthly payments, they aren't always the smartest financial decision.

Here's why.

Shorter Lease Terms

A shorter lease usually results in:

- Higher monthly payments

- Faster equity or ownership (depending on the lease type)

- Lower overall financing costs

- Greater flexibility to replace equipment sooner

Businesses often choose shorter terms when financing equipment expected to generate immediate revenue or retain its value for many years.

Longer Lease Terms

Longer lease terms typically provide:

- Lower monthly payments

- Improved monthly cash flow

- Easier budgeting

- More working capital available for payroll, inventory, and expansion

However, businesses should avoid extending a lease beyond the useful life of the equipment. If the equipment becomes outdated before the lease ends, you could still be making payments on an asset that's no longer delivering maximum value.

Pro Tip: Match your lease term to the expected life of the equipment—not just the lowest monthly payment.

Common Equipment Lease Payment Structures

Every business has different cash flow patterns. That's why many equipment financing companies offer flexible payment schedules designed to match how your business earns revenue.

Understanding these options can help you select a financing solution that works with your business instead of against it.

Level Payments

Level payments are the most common financing option.

Your monthly payment remains the same throughout the lease term, making budgeting simple and predictable.

This option works well for businesses with steady monthly revenue.

Examples include:

- Manufacturing facilities

- Medical practices

- Warehousing operations

- Commercial transportation companies

Seasonal Payments

Some businesses earn most of their income during certain times of the year.

Seasonal payment structures allow businesses to make lower payments during slower months and larger payments during peak revenue periods.

Industries that commonly benefit include:

- Construction

- Landscaping

- Agriculture

- Tree service companies

- Snow removal contractors

Matching payments to seasonal income helps preserve cash flow throughout the year.

Deferred Payments

Sometimes equipment begins generating revenue weeks or even months after delivery.

Deferred payment options allow businesses to postpone initial payments while equipment is installed, tested, or put into operation.

Deferred payments are popular for:

- Manufacturing equipment

- CNC machines

- Production lines

- Restaurant build-outs

- Medical equipment installations

This gives businesses time to begin earning revenue before regular payments start.

Step Payments

Step payment schedules begin with lower payments that gradually increase over time.

This option works well for:

- Start-up businesses

- Companies entering new markets

- Businesses expecting rapid growth

- Contractors beginning large projects

Instead of creating financial pressure immediately, payments increase as revenue grows.

Understanding End-of-Term Equipment Lease Options

One of the most important sections of any equipment lease agreement is what happens when your lease ends.

Many business owners focus only on the monthly payment and overlook their options at the conclusion of the lease.

Knowing your end-of-term choices ahead of time can save thousands of dollars and prevent unexpected surprises.

Most commercial equipment leases include one of the following options.

Fair Market Value (FMV) Lease

A Fair Market Value (FMV) lease provides the greatest flexibility.

At the end of the lease, you can typically:

- Return the equipment

- Purchase it at its current fair market value

- Renew the lease

- Upgrade to newer equipment

FMV leases are an excellent choice for equipment that becomes outdated quickly or businesses that like to upgrade regularly.

Common examples include:

- Computer systems

- Software

- Medical technology

- Printing equipment

- Fleet vehicles

- Technology-driven manufacturing equipment

Benefits of an FMV Lease include:

- Lower monthly payments

- Upgrade flexibility

- Reduced risk of owning obsolete equipment

- Preserved working capital

$1 Buyout Lease

A $1 Buyout Lease is designed for businesses that intend to own the equipment.

Throughout the lease, you're essentially financing the purchase of the equipment.

When the final payment is made, ownership transfers to your business for just $1.

This option is popular for:

- Excavators

- Dozers

- Dump trucks

- Tow trucks

- Forklifts

- Manufacturing machinery

- Commercial kitchen equipment

Businesses planning to keep equipment for many years often choose this structure because it provides ownership with predictable monthly payments.

FMV Lease vs. $1 Buyout Lease

| Feature | FMV Lease | $1 Buyout Lease |

|---|---|---|

| Monthly Payment | Lower | Higher |

| Ownership | Optional | Included |

| Upgrade Flexibility | Excellent | Limited |

| End-of-Term Options | Return, renew, purchase | Own equipment |

| Best For | Technology, fleets, rapidly changing equipment | Long-term equipment ownership |

Neither option is universally better. The right choice depends on how long you expect to use the equipment and whether ownership aligns with your business goals.

What Is Residual Value?

Residual value refers to the estimated value of the equipment at the end of the lease.

Residual value plays an important role in determining your monthly payment.

Generally speaking:

- Higher residual values often lead to lower monthly payments.

- Lower residual values typically result in higher monthly payments because you're financing more of the equipment's total cost.

Understanding residual value helps explain why two leases on similar equipment can have very different payment amounts.

Questions to Ask Before Signing an Equipment Lease

Before agreeing to any financing arrangement, ask your lender these important questions:

- How long is the lease?

- Are payments fixed or flexible?

- Is there a prepayment penalty?

- What happens if I need to upgrade equipment?

- Who is responsible for maintenance?

- What insurance is required?

- What are my options when the lease ends?

- Are there any additional fees?

- Can payments be customized around my cash flow?

- Which lease structure best fits my business goals?

Taking the time to understand these details can help you avoid costly surprises and choose financing that supports your company's long-term success.

At First Financial LLC, our financing specialists work closely with business owners to explain every lease option and help structure payments that fit each company's unique financial needs. Whether you're financing a single truck or expanding an entire fleet, we'll help you find a solution that supports your growth, not just your next purchase.

Equipment Lease Agreements: Maintenance, Insurance, and Other Important Terms

While monthly payments often receive the most attention, some of the most important parts of an equipment lease agreement are found in the fine print. Understanding your responsibilities before signing can help you avoid unexpected costs and ensure your equipment financing supports your business—not slows it down.

Who Is Responsible for Equipment Maintenance?

In most commercial equipment lease agreements, the business leasing the equipment is responsible for routine maintenance and repairs.

Keeping equipment in good working condition protects its value and helps minimize downtime. It also ensures that your business remains compliant with the terms of the lease agreement.

Maintenance responsibilities may include:

- Routine inspections

- Oil changes and fluid replacement

- Tire replacement

- Scheduled manufacturer service

- Preventive maintenance

- Minor repairs

- Keeping accurate service records

For example, if your company leases a rollback tow truck or an excavator, regular maintenance isn't just recommended—it helps extend the equipment's life and may be required by your lease agreement.

Failing to maintain equipment properly could result in additional charges or affect your end-of-term options.

Insurance Requirements for Equipment Leases

Most lenders require leased equipment to remain properly insured throughout the lease term.

Insurance protects both your business and the financing company if the equipment is damaged, stolen, or involved in an accident.

Depending on the type of equipment, you may need:

- Physical damage coverage

- Commercial auto insurance

- General liability insurance

- Inland marine insurance

- Property insurance

- Gap coverage (when applicable)

Before your lease begins, your financing company will explain the insurance requirements for your equipment.

Maintaining proper coverage throughout the lease helps protect your investment and keeps your financing agreement in good standing.

What Happens If Equipment Is Damaged?

Accidents happen—even to well-maintained equipment.

Your lease agreement should clearly explain:

- How damage must be reported

- Who pays for repairs

- Whether replacement equipment is covered

- Insurance claim procedures

- What happens if equipment is declared a total loss

Understanding these provisions ahead of time helps businesses respond quickly and minimize disruptions if unexpected events occur.

Returning Equipment at the End of an FMV Lease

If you've selected a Fair Market Value (FMV) lease, returning the equipment is often one of your end-of-term options.

Before returning equipment, it's important to understand the expected condition requirements.

Generally, equipment should be:

- Clean

- Fully operational

- Free from excessive wear

- Properly maintained

- Accompanied by any required manuals, keys, or accessories

Normal wear and tear is expected. However, excessive damage or missing components may result in additional charges.

Reviewing return requirements before signing the lease helps eliminate surprises later.

Understanding Default Clauses

No business plans to miss payments, but it's still important to understand what happens if financial challenges arise.

Default clauses explain the lender's rights if lease terms are not met.

Examples of default may include:

- Missed payments

- Failure to maintain insurance

- Unauthorized sale of equipment

- Bankruptcy

- Breach of lease terms

Depending on the agreement, consequences could include:

- Late fees

- Acceleration of remaining payments

- Repossession of equipment

- Collection activity

- Credit reporting

If your business encounters financial difficulties, communicating with your lender early is often the best approach. Many financing companies are willing to discuss solutions before problems escalate.

Can You Pay Off an Equipment Lease Early?

Many business owners ask whether they can pay off an equipment lease before the scheduled end date.

The answer depends on the financing agreement.

Some leases allow early payoff with little or no penalty, while others include fees designed to recover a portion of the remaining financing costs.

Before signing, ask your financing representative:

- Is early payoff allowed?

- Are there prepayment penalties?

- How is the payoff amount calculated?

- Will ownership transfer immediately after payoff?

Understanding these details gives you greater financial flexibility if your business grows faster than expected.

Real-World Equipment Leasing Examples

Every business has unique financing needs. Here are a few examples of how different lease structures can support different industries.

Tow Truck Company Expanding Its Fleet

A towing company wins several new municipal contracts and needs to add two rollback trucks.

Rather than paying cash, the owner chooses a $1 Buyout Lease to spread payments over five years while preserving working capital for payroll, insurance, and fuel.

At the end of the lease, the trucks become company-owned assets that continue generating revenue for years.

Construction Contractor Purchasing Heavy Equipment

A contractor needs a new excavator and compact track loader for multiple long-term projects.

Because cash flow varies throughout the year, seasonal payment options allow lower payments during slower winter months and higher payments during peak construction season.

This flexible financing structure helps maintain healthy cash flow without delaying equipment purchases.

Manufacturing Company Installing New Production Equipment

A manufacturer purchases an automated CNC machining center to increase production capacity.

Installation and employee training will take several months before the equipment reaches full production.

Deferred payment options allow the company to begin generating revenue before regular lease payments start.

Waste Management Business Growing Operations

A regional waste company is expanding into neighboring counties and needs vacuum trucks, hook-lift trucks, and roll-off containers.

Instead of tying up cash with large down payments, the company finances multiple pieces of equipment under customized payment schedules designed around projected growth.

This approach preserves capital for hiring drivers, purchasing inventory, and expanding operations.

How to Negotiate Better Equipment Lease Terms

Many business owners are surprised to learn that lease terms can often be customized.

Rather than focusing only on interest rates or monthly payments, consider discussing:

- Lease length

- Payment schedule

- Deferred payment options

- Seasonal payment plans

- End-of-term flexibility

- Upgrade options

- Early payoff provisions

- Down payment requirements

A financing solution tailored to your business can often provide more value than simply securing the lowest monthly payment.

Why Businesses Choose First Financial LLC

At First Financial LLC, we understand that no two businesses are exactly alike.

Whether you're financing one truck or an entire fleet, our team works to create financing solutions that align with your company's goals—not just standard loan terms.

We proudly finance equipment for businesses in industries including:

- Transportation

- Towing and Recovery

- Construction

- Waste Management

- Manufacturing

- Landscaping

- Agriculture

- Tree Care

- Municipal Services

- Warehousing

- Logistics

- Commercial Services

Our financing specialists take time to explain every option, answer your questions, and help you choose a lease structure that supports long-term success.

We offer competitive financing for both new and used equipment, flexible payment options, and a streamlined approval process designed to get your equipment working for you as quickly as possible.

Ready to Finance Your Next Piece of Equipment?

The right lease terms can make all the difference in preserving cash flow, supporting business growth, and maximizing the value of your investment.

Whether you're purchasing a tow truck, excavator, dump truck, manufacturing machine, restaurant equipment, or another commercial asset, First Financial LLC is here to help.

Contact our team today to discuss your equipment financing needs and discover customized leasing solutions built around your business.

Frequently Asked Questions About Equipment Lease Terms

1. What are equipment lease terms?

Equipment lease terms are the conditions of your financing agreement. They define the lease length, monthly payment amount, payment schedule, maintenance responsibilities, insurance requirements, end-of-term options, and any other conditions associated with leasing commercial equipment.

Understanding these terms before signing can help you choose a financing solution that aligns with your business goals.

2. What is the typical length of an equipment lease?

Most commercial equipment leases range from 24 to 84 months, depending on the type of equipment, its expected lifespan, and your business's financial objectives.

Heavy equipment and commercial vehicles often have longer lease terms, while technology and software may have shorter agreements due to faster obsolescence.

3. What is the difference between an FMV lease and a $1 Buyout lease?

A Fair Market Value (FMV) Lease offers lower monthly payments and allows you to return, renew, or purchase the equipment at its fair market value when the lease ends.

A $1 Buyout Lease is designed for businesses that want to own the equipment. After making all scheduled payments, ownership transfers for a nominal purchase price of $1.

The right option depends on whether you plan to keep the equipment long term or prefer the flexibility to upgrade.

4. Is leasing equipment better than buying?

There isn't a one-size-fits-all answer.

Leasing may be a better option if your business wants to:

- Preserve working capital

- Lower upfront costs

- Upgrade equipment more frequently

- Maintain predictable monthly payments

Buying may make sense if you plan to use the equipment for many years and prefer immediate ownership.

5. Can I finance used equipment?

Yes. Many businesses finance used equipment because it offers significant cost savings while still providing years of productive service.

At First Financial LLC, we help businesses finance both new and used commercial equipment across a wide range of industries.

6. Do equipment leases require a down payment?

Not always.

Depending on the equipment, credit profile, and financing program, businesses may qualify for little or no money down.

Your financing specialist can review available options based on your specific needs.

7. Can startups qualify for equipment financing?

Yes.

While established businesses often have more financing options, many startups can qualify based on factors such as:

- Personal credit

- Industry experience

- Equipment type

- Business plan

- Available collateral

If you're launching a new business, equipment financing may still be within reach.

8. What credit score is needed for equipment financing?

There isn't one minimum credit score that applies to every financing program.

Approval decisions often consider multiple factors, including:

- Personal and business credit

- Time in business

- Cash flow

- Equipment value

- Industry

- Overall financial strength

Even businesses with less-than-perfect credit may have financing options available.

9. Can lease payments be customized?

Yes.

Many lenders offer flexible payment structures, including:

- Seasonal payments

- Deferred payments

- Step payments

- Level monthly payments

Customizing your payment schedule can help improve cash flow and better align payments with your business's revenue cycle.

10. What types of equipment can be financed?

Commercial equipment financing is available for a wide variety of industries, including:

- Tow trucks

- Dump trucks

- Box trucks

- Semi trucks

- Excavators

- Skid steers

- Forklifts

- Manufacturing machinery

- Waste management equipment

- Vacuum trucks

- Trailers

- Modular buildings

- Commercial HVAC systems

If your business depends on specialized equipment, there's a good chance financing options are available.

11. Who is responsible for maintaining leased equipment?

In most commercial equipment leases, the business leasing the equipment is responsible for routine maintenance, repairs, and proper operation.

Following the manufacturer's maintenance schedule helps protect your investment and keeps the lease in good standing.

12. Can I pay off my equipment lease early?

Many financing agreements allow early payoff, although terms vary by lender.

Before signing your lease, ask whether:

- Early payoff is permitted

- Any prepayment penalties apply

- Ownership transfers immediately after payoff

Understanding these details provides greater flexibility if your financial situation changes.

13. What happens when my equipment lease ends?

Your options depend on the lease structure.

Depending on your agreement, you may be able to:

- Purchase the equipment

- Return the equipment

- Renew the lease

- Upgrade to newer equipment

Knowing your end-of-term options before signing helps you avoid surprises later.

14. Is equipment financing tax deductible?

In many cases, businesses may be able to deduct lease payments or depreciation expenses, depending on the financing structure and current tax laws.

Because every business is different, consult your accountant or tax advisor for guidance specific to your situation.

15. Why choose First Financial LLC for equipment financing?

At First Financial LLC, we understand that every business has unique financing needs.

We work with businesses across a wide range of industries to provide:

- Competitive financing solutions

- Flexible lease structures

- Financing for new and used equipment

- Fast approval decisions

- Personalized customer service

- Financing programs tailored to your business goals

Whether you're purchasing one piece of equipment or expanding an entire fleet, we're committed to helping you find the financing solution that best fits your business.

Final Thoughts

Choosing the right equipment lease involves more than comparing monthly payments. The lease structure you select can influence your cash flow, tax planning, equipment ownership, and long-term business growth.

By understanding lease terms, payment options, and end-of-term choices, you can make informed financing decisions with confidence.

If you're ready to finance heavy equipment, commercial vehicles, manufacturing machinery, restaurant equipment, or specialized business assets, the experienced team at First Financial LLC is here to help.

Request Your Free Equipment Financing Quote Today

Our financing specialists are ready to help you explore flexible lease options, competitive rates, and customized financing solutions designed to support your business's success. Contact First Financial LLC today to get started.

Submit an application now to get started: Credit Application | First Financial LLC | PA

📞 (866) 634-7786

📧 sales@firstfinllc.com

🌐 www.firstfinllc.com